Implementing Copula Methods for Multi-Asset Portfolio Risk Analysis

In modern portfolio risk management, understanding the joint behavior of multiple assets is crucial for accurate risk assessment. While traditional correlation-based approaches provide a simplified view of asset dependencies, copula methods offer a more sophisticated framework for modeling complex dependency structures between financial instruments. This article explores the practical implementation of copula-based techniques for multi-asset portfolio risk analysis in simulation environments.

Understanding Copulas in Financial Context

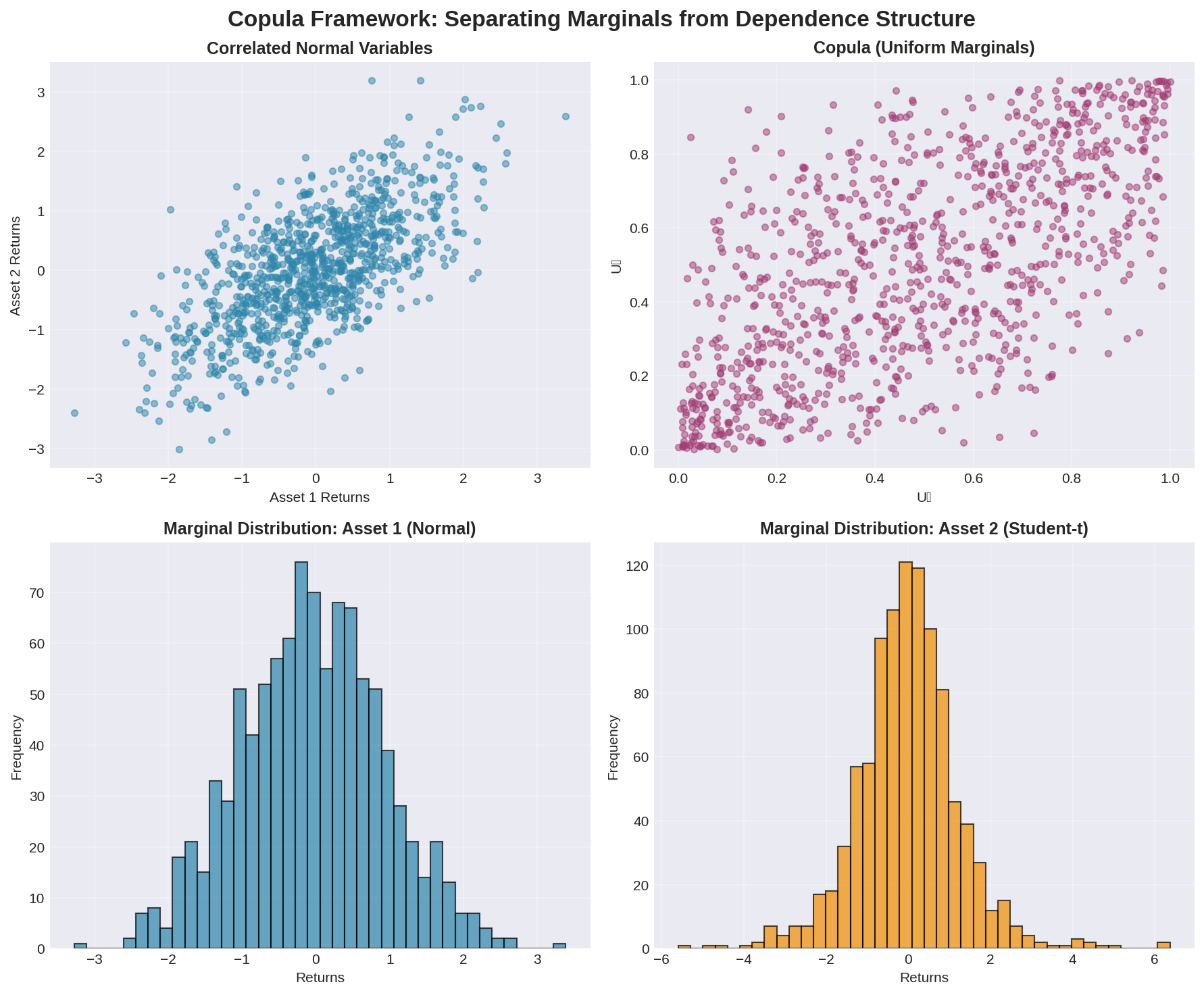

Copulas are mathematical functions that separate the marginal distributions of individual assets from their dependency structure. This separation is particularly valuable in finance, where asset returns often exhibit non-linear dependencies, tail dependence, and asymmetric correlation patterns that standard correlation matrices cannot capture. The Sklar's theorem forms the theoretical foundation, stating that any multivariate distribution can be decomposed into its marginal distributions and a copula function that describes their dependence.

For portfolio risk analysis, this means we can model each asset's return distribution independently (capturing individual characteristics like skewness and kurtosis) while simultaneously modeling how these assets move together during normal and extreme market conditions. This is especially critical for stress testing and tail risk assessment, where understanding joint extreme movements can mean the difference between accurate risk estimates and catastrophic underestimation.

Common Copula Families for Portfolio Analysis

Several copula families are widely used in financial applications, each capturing different dependency characteristics:

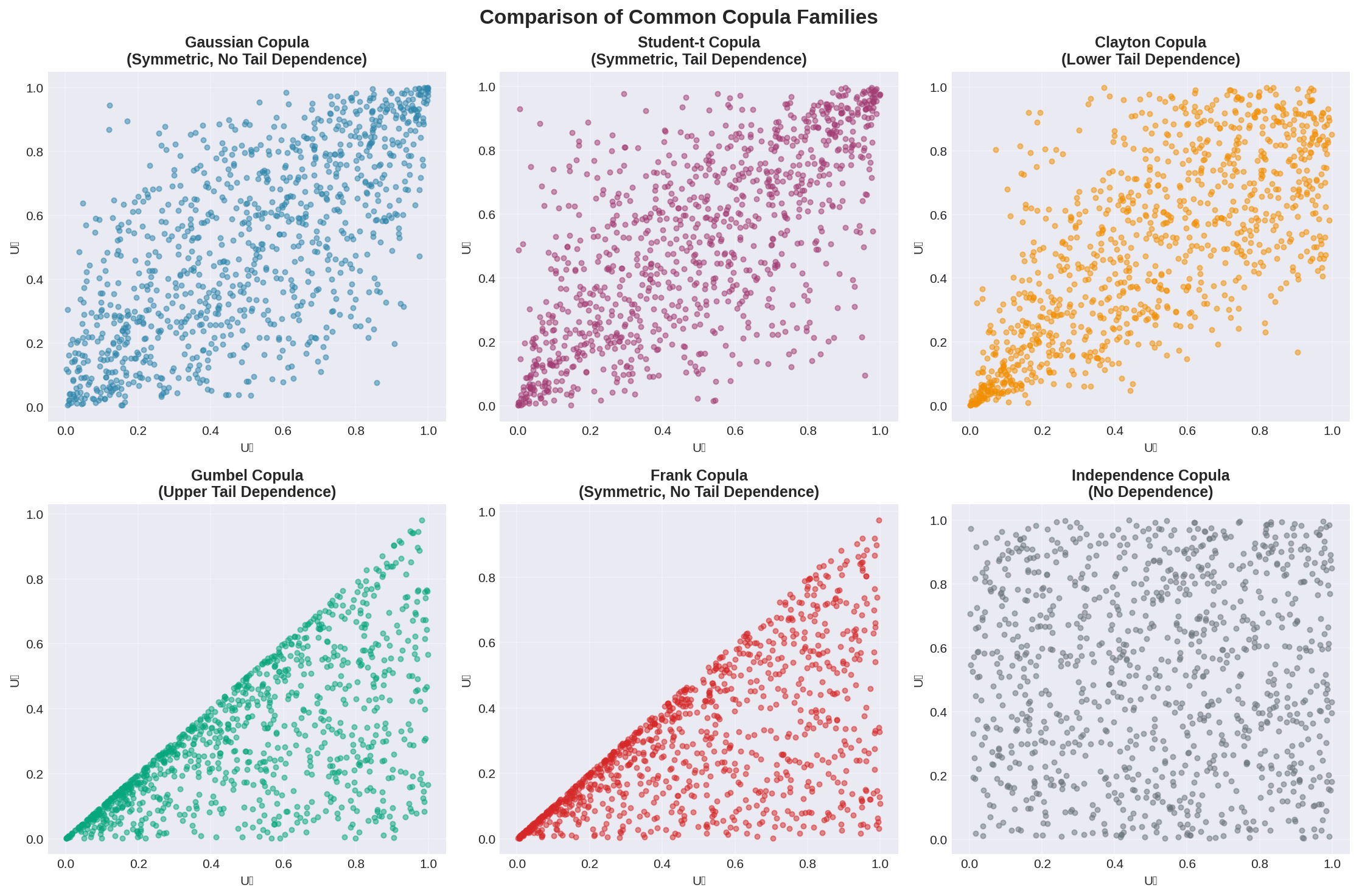

Gaussian Copula: Despite its limitations exposed during the 2008 financial crisis, the Gaussian copula remains useful for modeling symmetric dependencies in relatively stable market conditions. It's computationally efficient and provides a natural extension of correlation-based thinking.

Student's t-Copula: This copula introduces tail dependence through its degrees of freedom parameter, making it more suitable for capturing the tendency of assets to crash together during market stress. Lower degrees of freedom indicate stronger tail dependence, a critical feature for risk management.

Archimedean Copulas (Clayton, Gumbel, Frank): These single-parameter copulas offer computational simplicity while capturing asymmetric dependencies. The Clayton copula emphasizes lower tail dependence (joint crashes), while the Gumbel copula focuses on upper tail dependence (joint rallies). The Frank copula provides symmetric dependence without tail dependence.

Implementation Workflow

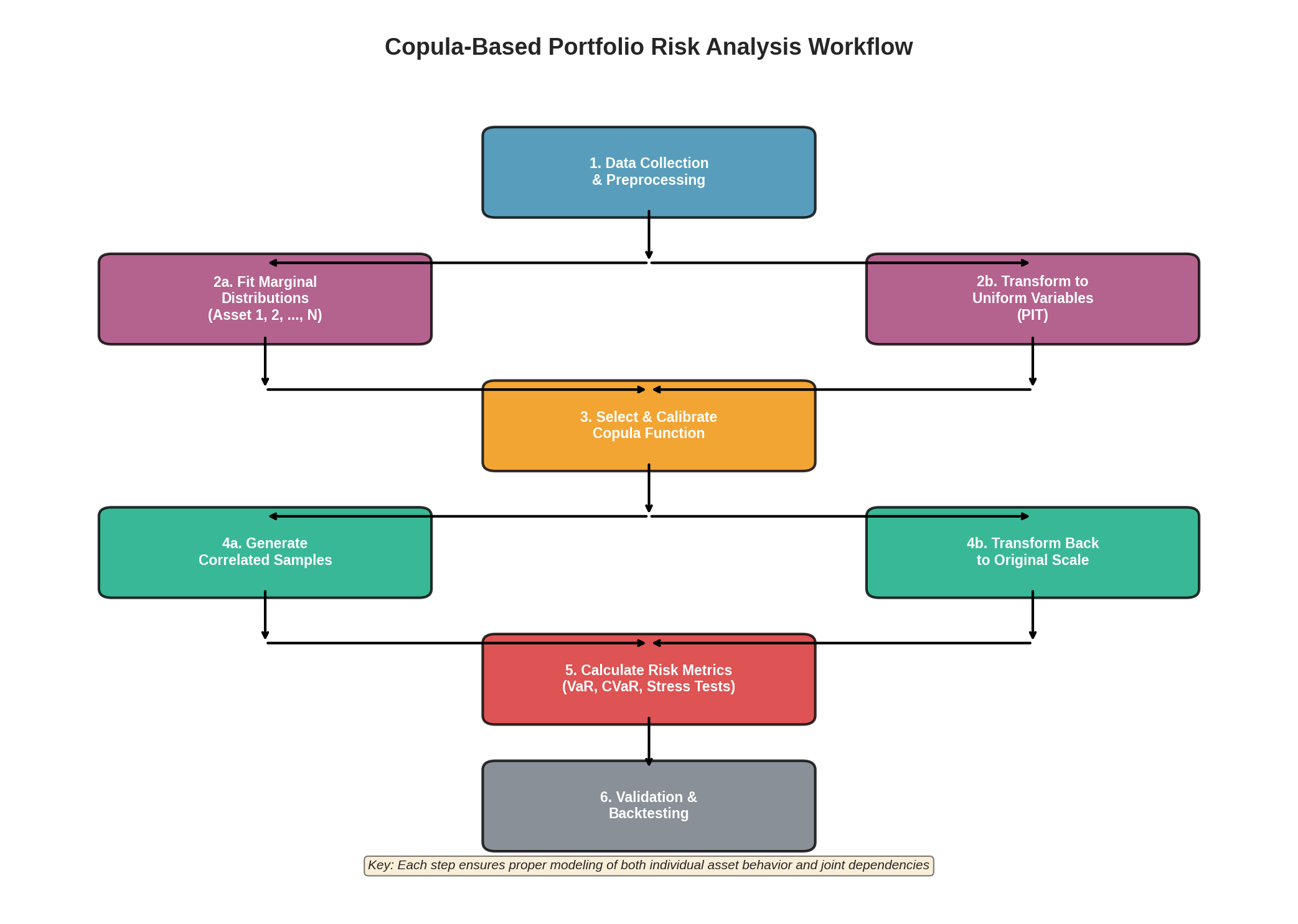

Implementing copula-based portfolio risk analysis typically follows these steps:

-

Marginal Distribution Fitting: For each asset, fit an appropriate distribution to historical returns. This might involve GARCH models for volatility clustering, or empirical distributions for non-parametric approaches.

-

Copula Selection and Calibration: Transform the fitted marginal distributions to uniform variables using probability integral transforms. Then, select and calibrate a copula family to these transformed variables. Information criteria (AIC, BIC) and goodness-of-fit tests help identify the most appropriate copula.

-

Simulation and Risk Metrics: Generate correlated uniform samples from the calibrated copula, then transform these back to the original return space using the inverse of the marginal distributions. Calculate portfolio-level risk metrics like Value-at-Risk (VaR), Conditional Value-at-Risk (CVaR), and stress scenarios.

-

Validation and Backtesting: Validate the copula model through backtesting against historical data and stress scenarios. Pay particular attention to tail behavior and crisis periods.

Practical Considerations

When implementing copula methods in production risk systems, several practical issues arise. High-dimensional copulas (portfolios with many assets) face the curse of dimensionality, often requiring vine copula structures or factor copula approaches to remain tractable. Model risk is significant—different copula choices can yield substantially different tail risk estimates, necessitating robust model validation and potentially ensemble approaches.

Computational efficiency matters for daily risk reporting. Pre-computing copula parameters and using efficient sampling algorithms (quasi-Monte Carlo, importance sampling) can reduce calculation times. Additionally, copula parameters should be regularly recalibrated as market conditions evolve, with particular attention during regime changes.

Integration with Risk Management Frameworks

Copula-based simulations integrate naturally into broader risk management workflows. They can feed into portfolio optimization routines that account for realistic dependency structures, stress testing frameworks that explore joint extreme scenarios, and regulatory capital calculations that require accurate tail risk estimates. Many commercial risk platforms now include copula capabilities, while open-source libraries in Python (scipy.stats, copulas) and R (copula package) provide accessible implementation tools.

The key advantage of copula methods lies in their flexibility to model the full spectrum of dependency patterns observed in financial markets, from normal times to crisis periods. For risk managers and quantitative analysts working with multi-asset portfolios, mastering copula techniques represents a significant step toward more robust and realistic risk assessment.

Further Resources

For deeper exploration of copula methods in finance, consult "Quantitative Risk Management" by McNeil, Frey, and Embrechts, which provides comprehensive theoretical and practical coverage. The R package documentation for 'copula' offers excellent implementation examples, while recent research papers on vine copulas and dynamic copulas extend these methods to even more complex scenarios.