Implementing Jump-Diffusion Models for Credit Risk Simulation

Credit risk modeling has evolved significantly beyond traditional Gaussian assumptions, particularly in capturing the sudden, discontinuous changes in credit quality that characterize real-world default events. Jump-diffusion models provide a powerful framework for simulating these dynamics, combining continuous diffusion processes with discrete jump components to more accurately represent credit deterioration and default scenarios.

Understanding Jump-Diffusion Dynamics in Credit Markets

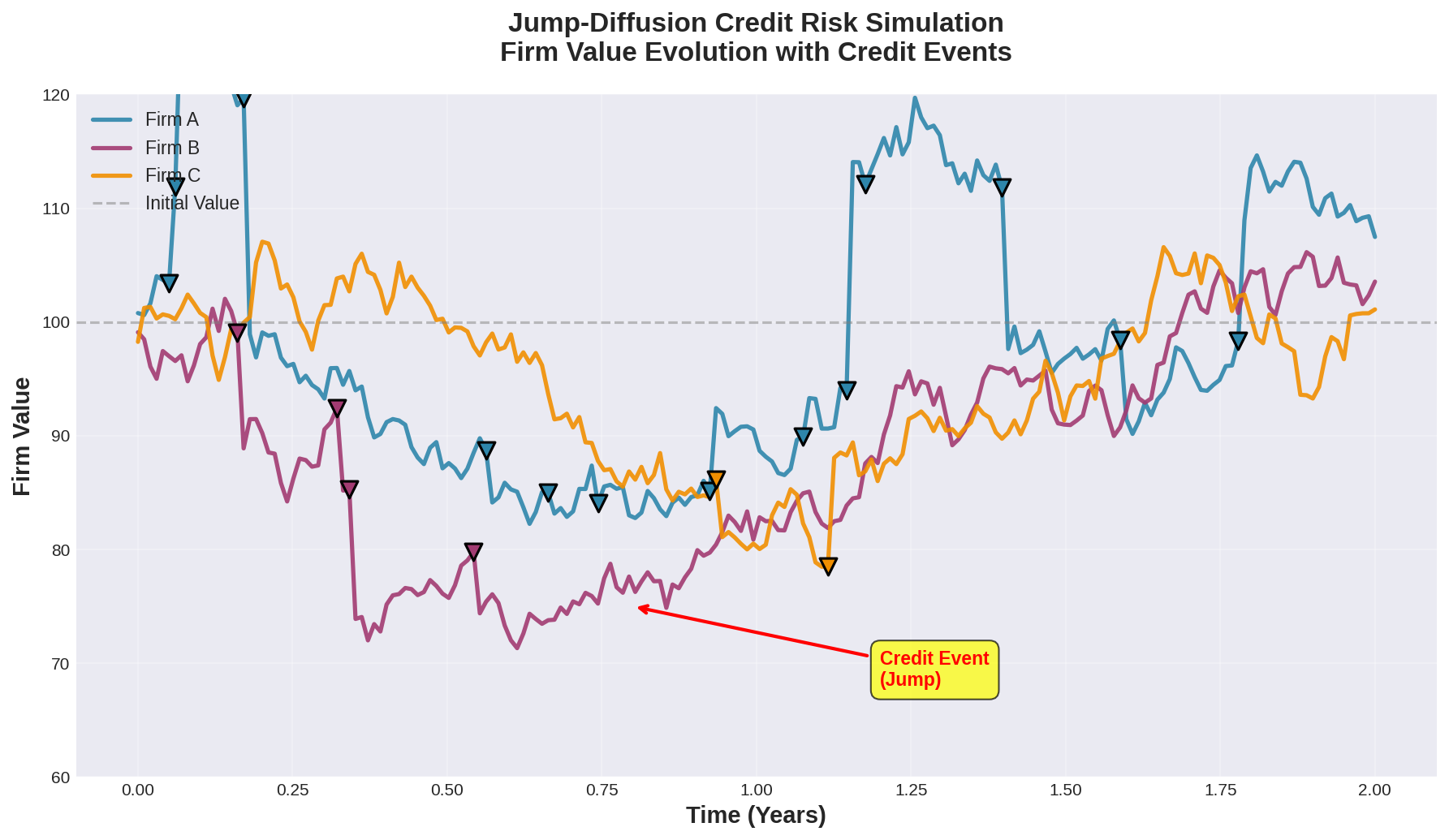

Traditional credit risk models based purely on continuous diffusion processes often fail to capture the abrupt nature of credit events. When a company announces unexpected losses, faces regulatory action, or experiences sudden market shocks, its credit spread can jump dramatically within hours or days—behavior that continuous models systematically underestimate.

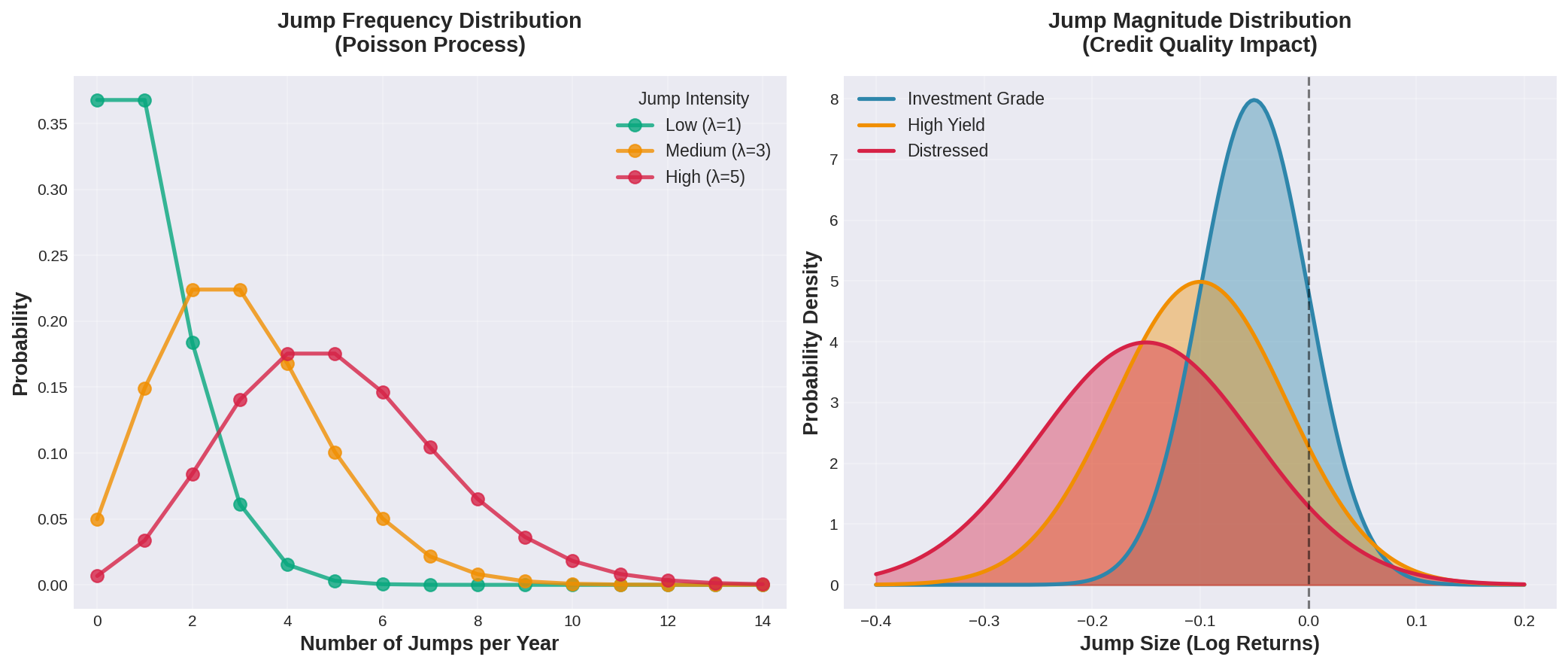

The Merton jump-diffusion framework extends the classic Black-Scholes-Merton approach by incorporating a Poisson process that governs the timing of jumps, combined with a distribution (typically log-normal or double-exponential) that determines jump magnitudes. This dual-component structure enables modelers to separately calibrate the baseline credit drift and volatility from the frequency and severity of credit shocks.

Technical Implementation Strategies

Implementing jump-diffusion models requires careful attention to both the continuous and discrete components. The asset value process typically follows:

dV = μV dt + σV dW + V(J-1) dN

where V represents firm value, μ is the drift rate, σ is volatility, dW is a Wiener process, J is the jump size (often log-normally distributed), and dN is a Poisson process with intensity λ.

For simulation purposes, the Euler-Maruyama scheme can handle the diffusion component, while the jump component requires generating Poisson-distributed jump times and sampling from the specified jump-size distribution. A critical implementation detail involves the time-step selection: while smaller steps improve diffusion accuracy, the Poisson process is memoryless, so jump timing remains statistically valid regardless of discretization.

Modern implementations often leverage GPU acceleration for large-scale credit portfolio simulations, where thousands of correlated obligors must be simulated simultaneously. The challenge lies in efficiently generating correlated jump processes—typically achieved through copula methods or factor models that link individual jump intensities to common systematic risk factors.

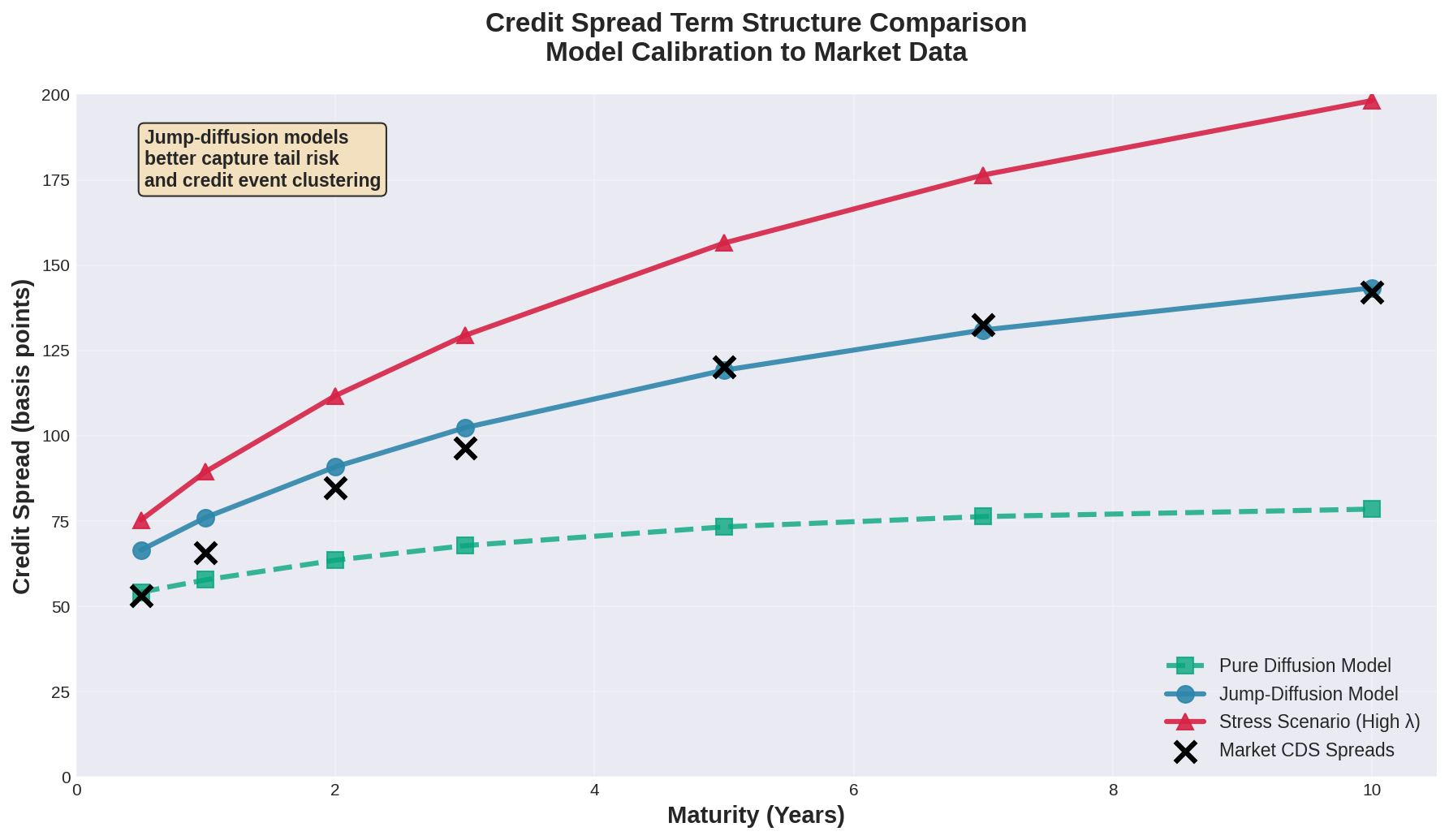

Calibration to Market Data

Calibrating jump-diffusion models to credit default swap (CDS) spreads and bond prices presents unique challenges. The model contains multiple parameters: drift, diffusion volatility, jump intensity, and jump-size distribution parameters. Maximum likelihood estimation from historical equity prices provides one approach, but market-implied calibration to current CDS term structures often yields more relevant forward-looking parameters.

A practical calibration workflow begins with extracting implied default probabilities from CDS spreads across multiple maturities. The jump intensity λ can be estimated from the frequency of significant credit rating downgrades or spread widening events in historical data. Jump-size parameters are then calibrated to match the observed term structure of credit spreads, recognizing that longer maturities incorporate more potential jump events.

Advanced practitioners often implement time-varying jump intensities that increase during periods of market stress, reflecting the empirical observation that credit events cluster during economic downturns. This can be achieved through regime-switching models or by making λ a function of macroeconomic indicators like the VIX or credit spread indices.

Applications in Stress Testing and Portfolio Management

Jump-diffusion models excel in stress testing scenarios where regulators and risk managers need to assess portfolio resilience to sudden credit deterioration. Unlike continuous models that may underestimate tail risk, jump-diffusion frameworks naturally generate the fat-tailed loss distributions observed in actual credit crises.

For portfolio credit risk, the correlation structure between jumps across different obligors becomes critical. Implementing a factor-based jump correlation structure—where individual jump intensities respond to common systematic factors—enables realistic simulation of contagion effects and systemic credit events. This approach has proven particularly valuable in analyzing structured credit products like CDOs, where correlation assumptions dramatically impact tranche valuations.

Counterparty credit risk modeling for derivatives portfolios represents another important application. Jump-diffusion models can simulate the joint evolution of counterparty creditworthiness and derivative exposure, capturing the "wrong-way risk" that arises when exposure increases precisely when counterparty credit quality deteriorates.

Computational Considerations and Best Practices

Efficient implementation requires balancing accuracy with computational feasibility. For single-name credit analysis, standard Monte Carlo with 10,000-50,000 paths typically suffices. Portfolio applications with hundreds or thousands of obligors demand more sophisticated approaches: quasi-Monte Carlo methods, importance sampling focused on tail scenarios, or hybrid analytical-numerical techniques that handle the diffusion component analytically while simulating jumps.

Validation remains essential. Comparing simulated credit spread distributions against historical data helps verify that the model captures realistic dynamics. Backtesting default predictions against actual default rates provides another critical validation check, particularly for the jump intensity calibration.

When implementing these models in production risk systems, consider maintaining separate parameter sets for different credit rating categories and industries, as jump characteristics vary significantly across credit quality levels and sectors. Investment-grade credits typically exhibit lower jump intensities but potentially larger jump sizes when events occur, while high-yield credits show more frequent but smaller jumps.

Further Resources

For deeper technical details on jump-diffusion implementation, consult Cont and Tankov's "Financial Modelling with Jump Processes" (Chapman & Hall, 2004). The QuantLib library provides open-source implementations of various jump-diffusion processes. For calibration methodologies, see the extensive literature on credit spread modeling in the Journal of Credit Risk and the Journal of Derivatives.

Practitioners seeking to implement these models should also review regulatory guidance on credit risk modeling from the Basel Committee on Banking Supervision, particularly regarding stress testing and model validation requirements for jump-based credit models.