Implementing Stochastic Differential Equations for Option Pricing Models

Stochastic Differential Equations (SDEs) form the mathematical backbone of modern option pricing theory, yet their practical implementation in simulation environments presents unique computational challenges. This article explores advanced techniques for implementing SDE-based option pricing models with a focus on numerical stability, convergence properties, and computational efficiency.

The Foundation: Black-Scholes-Merton Framework

The Black-Scholes-Merton model represents asset prices as geometric Brownian motion, expressed through the SDE:

dS(t) = μS(t)dt + σS(t)dW(t)

where S(t) is the asset price, μ is the drift coefficient, σ is the volatility, and dW(t) represents a Wiener process increment. While this equation appears straightforward, its numerical solution requires careful consideration of discretization schemes to avoid systematic bias and ensure convergence.

Discretization Schemes: Beyond Euler-Maruyama

The Euler-Maruyama method provides the simplest discretization approach, but it introduces significant bias for options with non-linear payoffs. The Milstein scheme offers superior convergence by incorporating second-order terms:

S(t+Δt) = S(t) + μS(t)Δt + σS(t)ΔW + 0.5σ²S(t)[(ΔW)² - Δt]

This additional term, derived from Itô's lemma, reduces the discretization error from O(Δt) to O(Δt²), dramatically improving accuracy for path-dependent options like Asian or barrier options. For practitioners implementing these schemes in production environments, the Milstein method typically reduces the required number of time steps by a factor of 4-10 while maintaining equivalent accuracy.

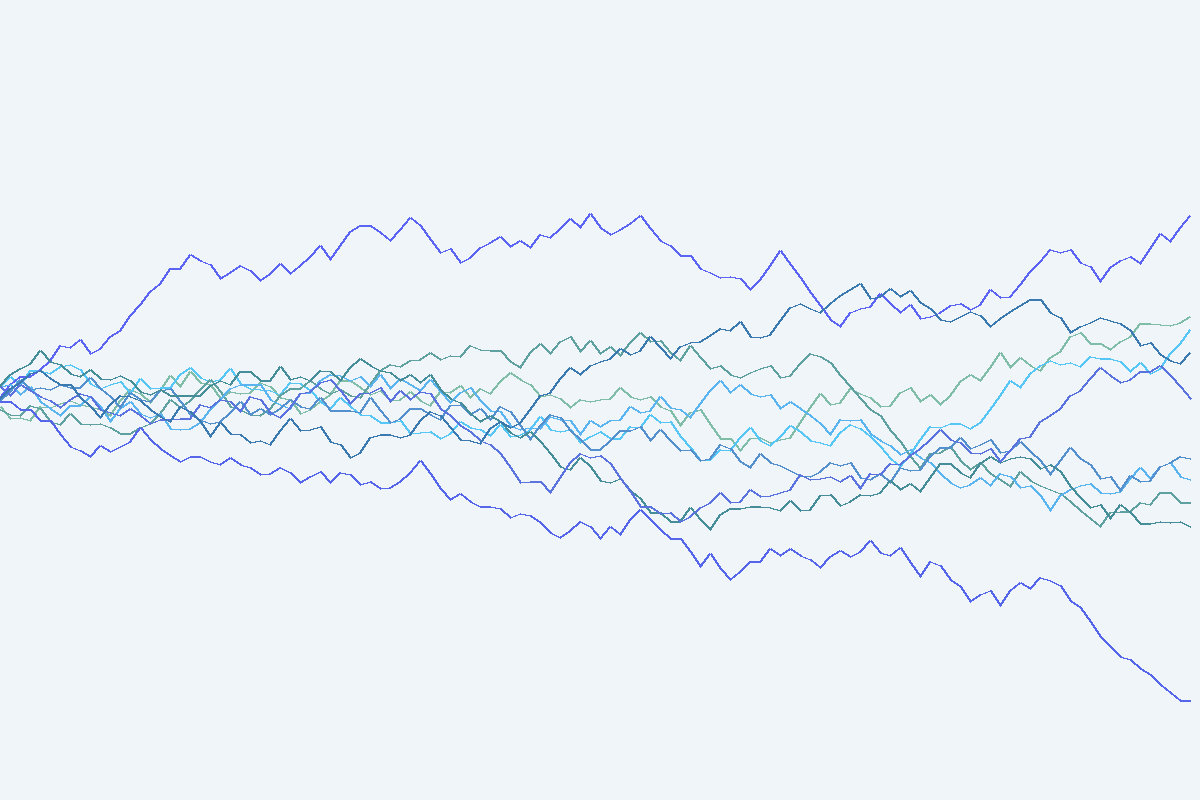

Multi-Asset Extensions: Cholesky Decomposition for Correlation

Real-world portfolios require multi-asset SDE systems with correlated Brownian motions. The standard approach employs Cholesky decomposition of the correlation matrix to generate correlated random variables. For an n-asset system with correlation matrix Ρ:

- Compute the Cholesky decomposition: Ρ = LL^T

- Generate independent standard normal variables Z₁, Z₂, ..., Zₙ

- Transform to correlated variables: W = LZ

This technique enables efficient simulation of basket options, spread options, and portfolio-level risk metrics. However, practitioners must ensure the correlation matrix remains positive definite throughout the simulation, particularly when using time-varying correlation structures.

Handling Stochastic Volatility: The Heston Model

The Heston model extends the Black-Scholes framework by treating volatility as a stochastic process:

dS(t) = μS(t)dt + √v(t)S(t)dW₁(t)

dv(t) = κ(θ - v(t))dt + ξ√v(t)dW₂(t)

where v(t) represents the variance process, κ is the mean-reversion speed, θ is the long-term variance, and ξ is the volatility of volatility. The correlation between dW₁ and dW₂ captures the leverage effect observed in equity markets.

Implementing the Heston model requires special attention to the Feller condition (2κθ > ξ²) to prevent the variance process from becoming negative. The full truncation scheme and reflection schemes offer different trade-offs between bias and computational efficiency. Recent research suggests the quadratic-exponential (QE) scheme provides optimal balance for most parameter regimes.

Variance Reduction Through Antithetic Variates

When pricing European options under SDE models, antithetic variates can reduce variance by 40-60% with minimal computational overhead. For each simulated path with Brownian increments ΔW, simultaneously compute a path with -ΔW. The average of the two payoffs provides a variance-reduced estimate.

This technique proves particularly effective for options with monotonic payoff functions. However, for path-dependent options with complex payoff structures, the variance reduction benefit diminishes and may require more sophisticated control variate approaches.

Practical Implementation Considerations

Modern SDE implementations should leverage vectorized operations and GPU acceleration for large-scale simulations. Python libraries like NumPy and CuPy enable efficient batch processing of thousands of paths simultaneously. For production systems, consider:

- Adaptive time-stepping: Reduce Δt near barriers or discontinuities

- Moment matching: Ensure simulated paths preserve analytical moments

- Convergence testing: Validate results against closed-form solutions when available

- Numerical stability: Monitor for overflow in exponential terms and underflow in probability calculations

Integration with Risk Management Systems

SDE-based pricing models integrate naturally with Value-at-Risk (VaR) and Expected Shortfall (ES) calculations. By simulating full price distributions rather than point estimates, risk managers gain insight into tail behavior and extreme scenarios. The computational cost of SDE simulation has decreased dramatically with modern hardware, making real-time risk calculations feasible for portfolios containing thousands of positions.

Conclusion

Implementing SDE-based option pricing models requires balancing mathematical rigor with computational pragmatism. The choice of discretization scheme, variance reduction techniques, and numerical stability measures significantly impacts both accuracy and performance. As computational resources continue to expand, SDE methods will increasingly replace closed-form approximations, enabling more realistic modeling of complex derivatives and portfolio-level risk.

For practitioners seeking to implement these techniques, open-source libraries like QuantLib provide battle-tested implementations, while commercial platforms like MATLAB's Financial Toolbox offer integrated environments for rapid prototyping and production deployment.

Further Reading

- Glasserman, P. (2003). Monte Carlo Methods in Financial Engineering. Springer.

- Kloeden, P.E., & Platen, E. (1992). Numerical Solution of Stochastic Differential Equations. Springer.

- QuantLib Documentation: https://www.quantlib.org/

- Heston, S.L. (1993). "A Closed-Form Solution for Options with Stochastic Volatility." Review of Financial Studies, 6(2), 327-343.