Monte Carlo Simulation: Advanced Financial Risk Modeling and Decision Analysis

The Monte Carlo simulation, often referred to as Monte Carlo methods or Monte Carlo experiments, represents a broad and powerful class of computational algorithms that fundamentally rely on repeated random sampling to achieve numerical results. This technique is designed to tackle problems that, while potentially deterministic in principle, become intractable due to inherent uncertainties and complexities.

Overview and Historical Context

The method's name is famously derived from the Monte Carlo Casino in Monaco, a nod to the element of chance and randomness central to its operation. It was inspired by the gambling habits of mathematician Stanisław Ulam's uncle, who, along with John von Neumann, pioneered the method in the 1940s for studying neutron diffusion.

In the realm of finance, Monte Carlo simulation stands as an indispensable statistical technique for modeling and analyzing the profound impact of risk and uncertainty on financial decision-making. By generating and evaluating thousands, or even millions, of possible outcomes, it empowers businesses and investors to make highly informed decisions, moving beyond singular deterministic forecasts to understand the full spectrum of potential results and their associated probabilities.

This comprehensive approach provides a probabilistic view of potential outcomes, making it one of the most effective tools for risk assessment and financial forecasting.

Core Concepts and Mechanism

At its heart, Monte Carlo simulation is a computational algorithm that leverages random sampling and statistical analysis to predict a range of possible outcomes, making it an essential tool for decision-making in uncertain environments across various fields, including finance, engineering, and science.

Key Components of Monte Carlo Simulation

Monte Carlo simulations are built upon the interplay of three fundamental elements: input variables, mathematical models, and output variables. These components are critical in determining both the accuracy and dependability of simulation outcomes.

1. Input Variables

These are the foundational elements that encapsulate the inherent uncertainties needing to be incorporated into the model. They represent the different factors that can influence the output, such as market volatility, interest rates, company earnings reports, or geopolitical events in financial contexts. Input variables can adopt various statistical distributions:

- Uniform Distribution: Implies an equal probability for all potential results within a defined range. For instance, when rolling a standard six-sided die, each side has the same chance of landing face up.

- Triangular Distribution: Employs minimum, maximum, and a most likely value to characterize random variables. This is often used when there's an identifiable range of potential outcomes but also a central anticipated outcome.

- Normal Distribution: A frequently utilized probability distribution, characterized by a symmetric bell curve where data points predominantly congregate around the mean value. It is especially valuable for simulating variables that exhibit a natural tendency to cluster around an average point, like financial market returns.

- Lognormal and Binomial Distributions: Also commonly used, particularly for modeling stock prices (lognormal) or discrete events (binomial).

2. Mathematical Models

These act as the foundational equations connecting input variables to output variables within a Monte Carlo simulation. They delineate the impact of variable changes on results, offering a structure through which the simulation can compute likely outcomes using established mathematical methods. For example, in financial simulations, such models might substitute actual revenue and expense figures with potential values derived from probability distributions.

3. Output Variables

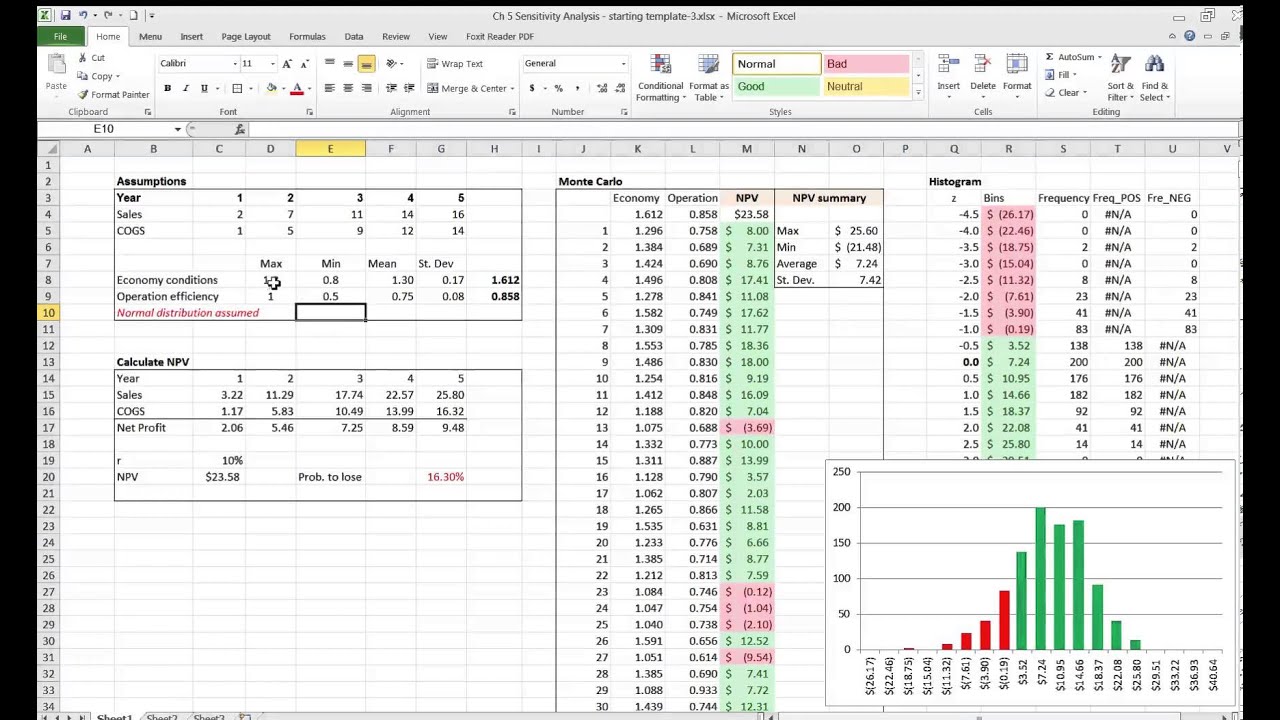

These are the results produced by Monte Carlo simulations, encompassing a variety of potential outcomes and their corresponding likelihoods. These outputs can be depicted in the form of charts or histograms, offering an easily interpretable method to display the findings. Output variables might include aspects such as portfolio returns, project NPV, or forecasted sales figures derived through Monte Carlo evaluation.

Step-by-Step Process

The execution of a Monte Carlo simulation encompasses a systematic series of essential steps:

- Define the Problem or Scenario: Precisely define the financial problem or scenario that the simulation aims to address.

- Identify Key Variables: Determine the variables that significantly influence the outcomes, such as stock prices, interest rates, or economic conditions.

- Assign Probability Distributions: Based on historical data or well-researched assumptions, assign appropriate probability distributions to each of the identified variables.

- Create the Model: Formulate the mathematical model that correlates the input variables with the output variables.

- Generate Random Inputs: Use random sampling to generate values for the variables based on their assigned probability distributions.

- Run Simulations: Conduct thousands, or even millions, of iterations of the simulation. Each iteration involves a new set of randomly generated inputs, and the mathematical model computes a corresponding output.

- Analyze Results: Apply statistical tools to scrutinize the distribution of the results, calculating summary statistics and estimating the probability of different scenarios.

Features of Monte Carlo Simulation in Finance

Monte Carlo simulation offers several distinct features that make it a powerful and versatile tool in financial analysis and risk management.

Probabilistic View and Handling Uncertainty

Unlike traditional static or deterministic models that provide a single point estimate, Monte Carlo simulation offers a probabilistic view of potential outcomes. It is adept at modeling the uncertainty inherent in financial markets by accounting for the variability of outcomes, mirroring the complex nature of real-life scenarios.

This includes forecasting potential fluctuations in stock prices by taking into account diverse market variables, interest rates, or economic conditions. The ability to simulate complex systems and envision numerous prospective scenarios showcases the robust capability inherent in Monte Carlo methods.

Comprehensive Risk Assessment Tool

Monte Carlo simulation is a valuable tool for financial professionals to understand and manage risk. It helps businesses and investors make informed decisions by understanding the range of potential results and their probabilities. It is widely used to measure and manage various financial risks, including Value at Risk (VaR) and stress testing.

By simulating market movements, it can estimate the probability and size of potential portfolio losses. This technique helps financial professionals visualize potential outcomes, evaluate risk, and make more informed decisions by running simulations that incorporate a wide range of variables.

Applicability to Complex Problems

Monte Carlo simulation is particularly beneficial when addressing deterministic problems that necessitate factoring in variations. It can handle complex and nonlinear models where analytical solutions are not available or are too complex to obtain. This makes it suitable for valuing complex financial derivatives where closed-form solutions are impractical.

By sampling across different ranges of input variability, Monte Carlo methods spawn numerous hypothetical future states that enhance decision-making bolstered by deterministic mathematical approaches.

Enhanced Decision-Making and Transparency

The primary advantage of employing these simulations lies in their capacity to manage substantial uncertainty and yield an array of likely outcomes instead of merely presenting a singular forecasted value. Monte Carlo simulations offer a critical advantage in creating greater transparency than traditional deterministic predictions.

They use the power of computing to produce tens of thousands of hypothetical scenarios, thereby enhancing understanding beyond what historical data alone can reveal and offering an expansive view of possible futures. This helps investors and managers weigh risks and rewards more effectively.

Sensitivity Analysis Capability

Once Monte Carlo simulations have been executed and results analyzed, conducting sensitivity analysis enhances the understanding of which variables significantly influence outcomes. This analysis is crucial for financial strategists who need to pinpoint which assumptions warrant the closest scrutiny.

By systematically altering one variable at a time and observing the impact on simulation results, analysts can identify the most influential factors within the model. This approach helps in isolating the elements that could introduce volatility into financial strategies.

Applications in Finance

Monte Carlo simulation is commonly applied across various financial domains to model and predict a range of outcomes, enabling informed decision-making and effective risk management.

Portfolio Risk and Return Analysis

This is a primary application where Monte Carlo simulation models the potential performance of investment portfolios under various market conditions. It can simulate the annual returns of a portfolio over extended periods, accounting for historical volatility and correlations between assets.

This allows for determining probabilities for outcomes like exceeding a specific return threshold or incurring losses, helping managers optimize asset allocation strategies. The simulation can incorporate complex relationships between different asset classes and market factors.

Financial Planning and Retirement

Monte Carlo helps individuals and financial advisors assess the likelihood of a retirement plan's success. It can simulate a retiree's investment growth and withdrawals under different market scenarios, analyzing probabilities of the portfolio lasting a given time frame, such as 30 years.

This application is particularly valuable for understanding the sustainability of withdrawal rates and the impact of market volatility on long-term financial security.

Option Pricing and Derivatives Valuation

Monte Carlo methods are extensively used to value complex financial derivatives, especially when closed-form solutions are impractical or for instruments with multiple sources of uncertainty. It simulates the price path of an underlying stock to estimate the fair value of an option, accounting for factors like underlying asset volatility and interest rate changes.

This is particularly useful for exotic options, path-dependent derivatives, and instruments with complex payoff structures that cannot be easily valued using traditional analytical methods.

Risk Management (VaR and Stress Testing)

Financial institutions widely use Monte Carlo simulation to measure and manage various risks, including Value at Risk (VaR) and stress testing. It simulates market movements to estimate the probability and size of potential portfolio losses, helping institutions assess the adequacy of their risk management strategies.

It is also applied in operational risk assessment, where it models and measures risks inherent in a firm's operational processes, creating a complete risk profile. This includes modeling credit risk, market risk, and operational risk scenarios.

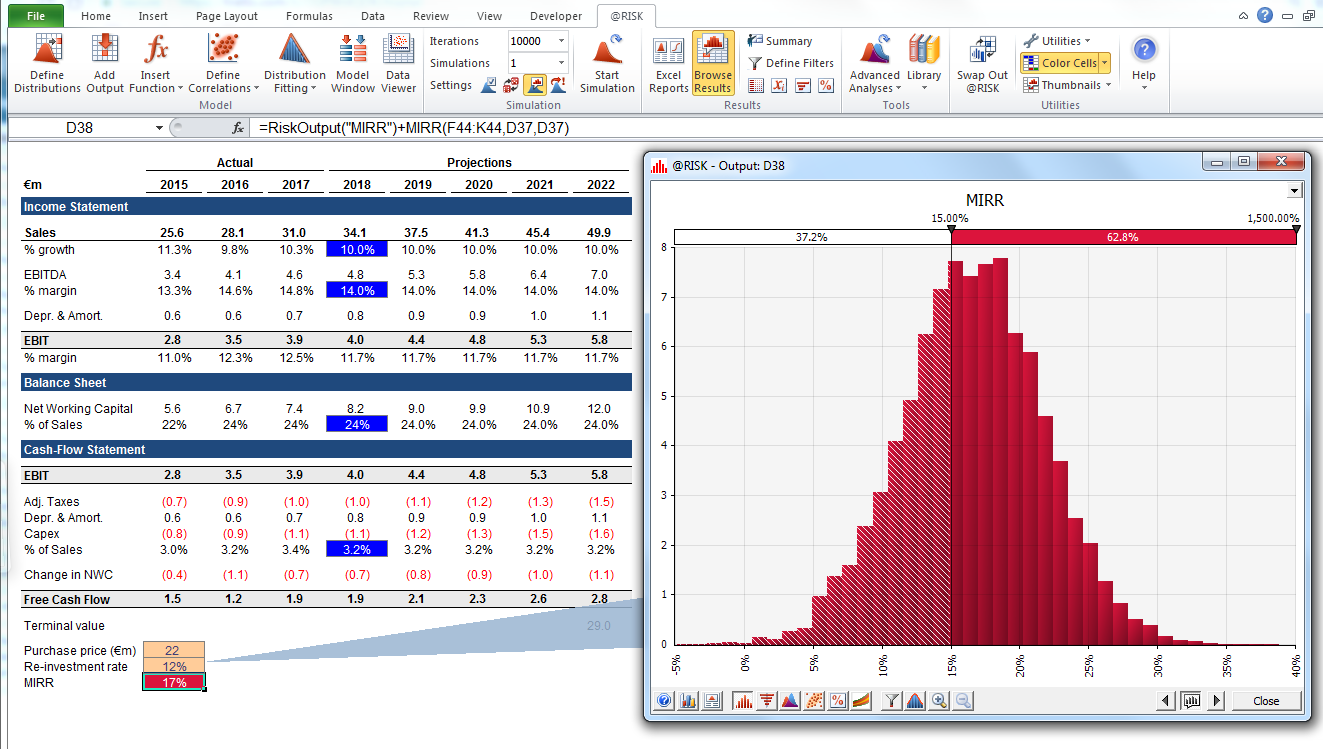

Capital Budgeting and Project Valuation

Monte Carlo simulation is applied to assess the risks and returns of capital projects or mergers. It simulates future cash flows under different economic scenarios to evaluate a project's Net Present Value (NPV) or Internal Rate of Return (IRR), enabling firms to make informed investment decisions.

This application helps in exploring a range of potential cost and revenue scenarios, accounting for uncertainties in market conditions, regulatory changes, and operational factors.

Financial Forecasting

It serves as a powerful approach to capture and represent uncertainty, providing a range of outcomes to support decision-makers in risk management. It can handle virtually any type of probability distribution, including those hard to model with other tools.

This allows forecasters to consider sudden market shifts, economic factors, or company-specific events that might impact financial performance. The simulation can incorporate complex dependencies and correlations between different economic variables.

Benefits and Limitations

Benefits of Using Monte Carlo Simulation

- Incorporates Uncertainty and Variability: It models variability in inputs to reflect real-world complexities, providing a more accurate depiction of inherent uncertainty within forecasting models.

- Provides a Range of Outcomes: It highlights not just average results but also best-case and worst-case scenarios, offering an expansive view of possible futures. This allows for a comprehensive, randomized outcome that gives financial analysts a broader perspective.

- Enhances Decision-Making: By providing critical insights into potential outcomes and their probabilities, it helps investors and managers weigh risks and rewards more effectively, leading to more informed and strategic decisions.

- Applicable to Complex Problems: It handles situations where analytical solutions are impractical or too complex, making it suitable for modeling intricate financial instruments and scenarios.

- Greater Transparency: Monte Carlo simulations offer greater transparency than traditional deterministic predictions by producing tens of thousands of hypothetical scenarios, enhancing understanding beyond historical data.

- Efficiency: This stochastic technique harnesses the power of computing to perform hundreds, or even thousands, of calculations instantaneously, offering swift, comprehensive risk assessments.

Limitations of Monte Carlo Simulation

- Assumption Sensitivity: The accuracy of results heavily depends on the quality and accuracy of input assumptions, such as probability distributions and correlations. If unreliable or inaccurate data is used, the output would be similarly flawed.

- Computational Intensity: Monte Carlo simulations require a large number of iterations to arrive at a reliable result, which can demand significant computational power and time. The level of complexity increases with the number of variables involved.

- Misinterpretation Risks: The outcomes represent probabilities, which can sometimes be misunderstood or misinterpreted. A high probability does not guarantee an outcome, and low-probability events can still occur.

- Limitations with Certain Types of Financial Data: Monte Carlo simulations are based on the assumption that the future will, to an extent, resemble the past. However, major economic or financial shocks, shifts in market dynamics, or changes in fiscal or monetary policy can result in future scenarios that differ significantly from historical data.

- Model Risk: Errors in the underlying mathematical model could lead to misleading results. It may not capture all sources of uncertainty and variability in the model, leading to biased or incomplete results.

Best Practices for Implementation

To ensure the accuracy, reliability, and effectiveness of Monte Carlo simulations, several best practices should be followed:

Data Quality and Model Design

Use Quality Data: Base assumptions and distributions on reliable historical data or well-researched estimates. Inaccurate inputs will lead to inaccurate simulation results.

Choose the Right Probability Distribution: Carefully consider the underlying data and select the distribution that best fits the data. This involves a blend of statistical acumen and an understanding of the financial environment.

Address Correlated Variables: When variables are correlated, it can be challenging to accurately model their joint distribution. It is essential to carefully consider the relationships between variables and incorporate appropriate correlation structures in the simulation.

Simulation Configuration

Run Sufficient Iterations: More iterations generally improve the accuracy of results, though they increase computational demands. It is essential to carefully consider the sample size needed for the specific simulation and ensure it is large enough to provide accurate results.

Monitor Convergence: Diligently track the convergence of the simulation to know when it's time to stop, preventing 'overrunning' the model. Techniques like the R-hat statistic can help.

Test Sensitivity: Explore how changes in input assumptions affect outcomes. By systematically altering one variable at a time and observing the impact, analysts can identify the most influential factors and understand the robustness of the model's conclusions.

Validation and Integration

Model Validation: Validate the model against real-world data to ensure that the simulation accurately represents the underlying system. Without proper validation, the results may not be reliable.

Combine with Other Methods: Use Monte Carlo alongside scenario analysis and stress testing for robust decision-making. It should be used in conjunction with other methods and not treated as the ultimate predictor of future events.

Clear Documentation: Models should be transparent, with clear documentation of assumptions, inputs, and outputs.

Advanced Techniques

To enhance the accuracy and efficiency of Monte Carlo simulations, several advanced techniques are employed:

Variance Reduction Techniques

Antithetic Variates: Involves pairing two opposite random variables and using their average to cancel out extremes, effectively mirroring the initial random variable to reduce overall variance.

Control Variates: Uses a second, theoretically simpler, Monte Carlo simulation to correct the initial model, subtly incorporating related variables to drive down variance and improve the computational process.

Quasi-Random Sequences

Instead of typical randomly generated numbers, quasi-random sequences aim to reduce clustering, which can compromise simulation accuracy. They ensure a more regular and homogeneous distribution across the sampling space, making simulations more accurate and faster in convergence. Examples include the Sobol sequence and the Halton sequence.

Convergence Monitoring

This complex feature helps analysts know when to stop the simulation by tracking its convergence, preventing the model from running long after it has stabilized. Looking at the mean square error or using techniques like the R-hat statistic can help in effectively monitoring convergence.

Tools and Software

A variety of tools and software are available to facilitate Monte Carlo simulations:

Excel Add-Ons: Tools like @Risk or Crystal Ball integrate Monte Carlo Simulation directly with Microsoft Excel, making it accessible for users familiar with spreadsheets.

Python Libraries: Libraries such as NumPy, SciPy, and PyMC3 allow for detailed modeling and simulation, offering flexibility and power for more complex scenarios.

Specialized Software: Platforms like MATLAB and R provide advanced capabilities for Monte Carlo Simulation, often preferred for their statistical and computational power in academic and professional settings.

Conclusion

Monte Carlo simulation is a versatile and powerful tool for financial decision-making, enabling individuals and organizations to model uncertainty and make informed choices. By modeling the inherent uncertainty and randomness of financial processes, these simulations provide valuable insights for better decision-making, whether analyzing portfolio risks, valuing options, or planning for retirement.

Its ability to provide a comprehensive, probabilistic view of potential outcomes makes it an indispensable asset in navigating the complexities and inherent risks of the financial world. The technique's flexibility in handling complex, nonlinear relationships and its capacity to incorporate multiple sources of uncertainty make it particularly valuable in today's dynamic financial environment.

As financial markets become increasingly complex and interconnected, Monte Carlo simulation continues to evolve as a critical tool for risk management, investment analysis, and strategic planning. Its integration with modern computing technologies and advanced statistical methods ensures its continued relevance and effectiveness in addressing the challenges of contemporary finance.