Variance Reduction Techniques in Financial Monte Carlo Simulations

Monte Carlo simulation has become indispensable in quantitative finance, but computational efficiency remains a critical challenge. While basic Monte Carlo methods provide accurate results, they often require millions of iterations to achieve acceptable convergence. Variance reduction techniques offer a powerful solution, dramatically improving simulation efficiency without sacrificing accuracy.

Understanding the Computational Challenge

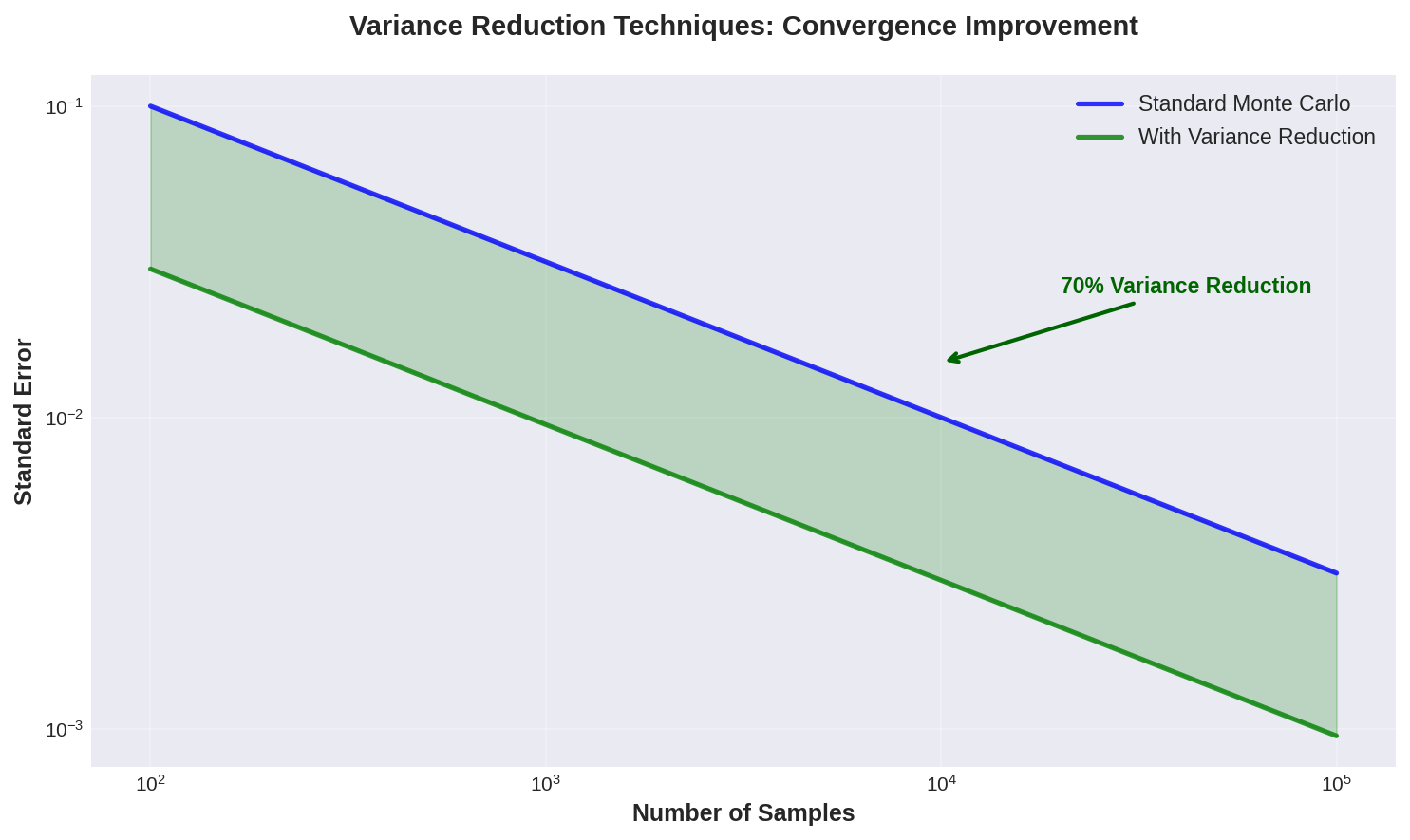

Standard Monte Carlo simulations suffer from slow convergence rates, with error decreasing proportionally to the square root of the number of samples. For complex derivatives pricing or portfolio risk calculations, this can translate to hours or even days of computation time. Variance reduction techniques address this fundamental limitation by exploiting structural properties of the problem to reduce the variance of estimators.

Antithetic Variates: Exploiting Symmetry

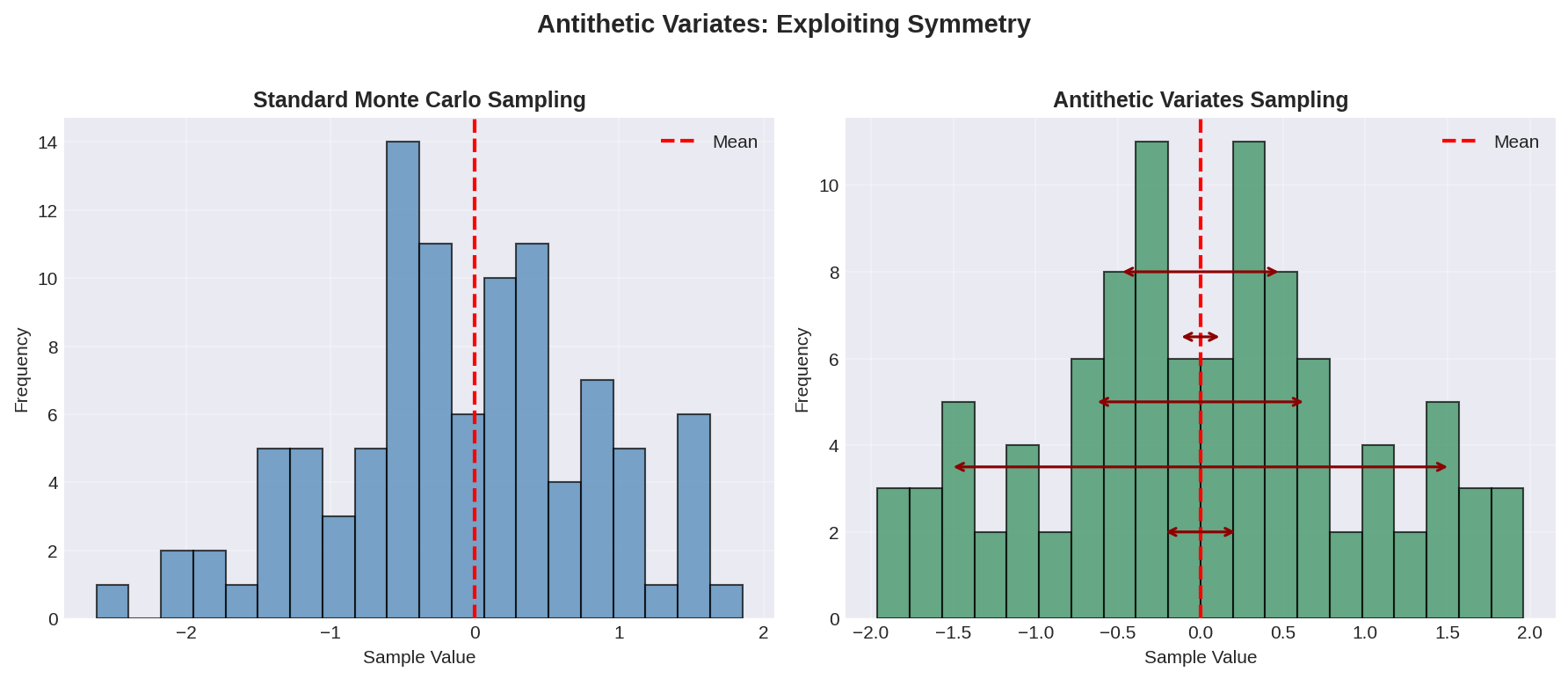

Antithetic variates represent one of the most straightforward yet effective variance reduction methods. Instead of generating independent random samples, this technique generates pairs of negatively correlated samples. For each random variable Z drawn from a standard normal distribution, we also use -Z. This approach leverages the symmetry of many financial models.

In practice, when pricing European options using geometric Brownian motion, antithetic variates can reduce variance by 30-50% with virtually no additional computational cost. The technique works particularly well when the payoff function is monotonic in the underlying random variables. Implementation requires minimal code changes—simply generate half the required samples and create their antithetic counterparts.

Control Variates: Leveraging Known Solutions

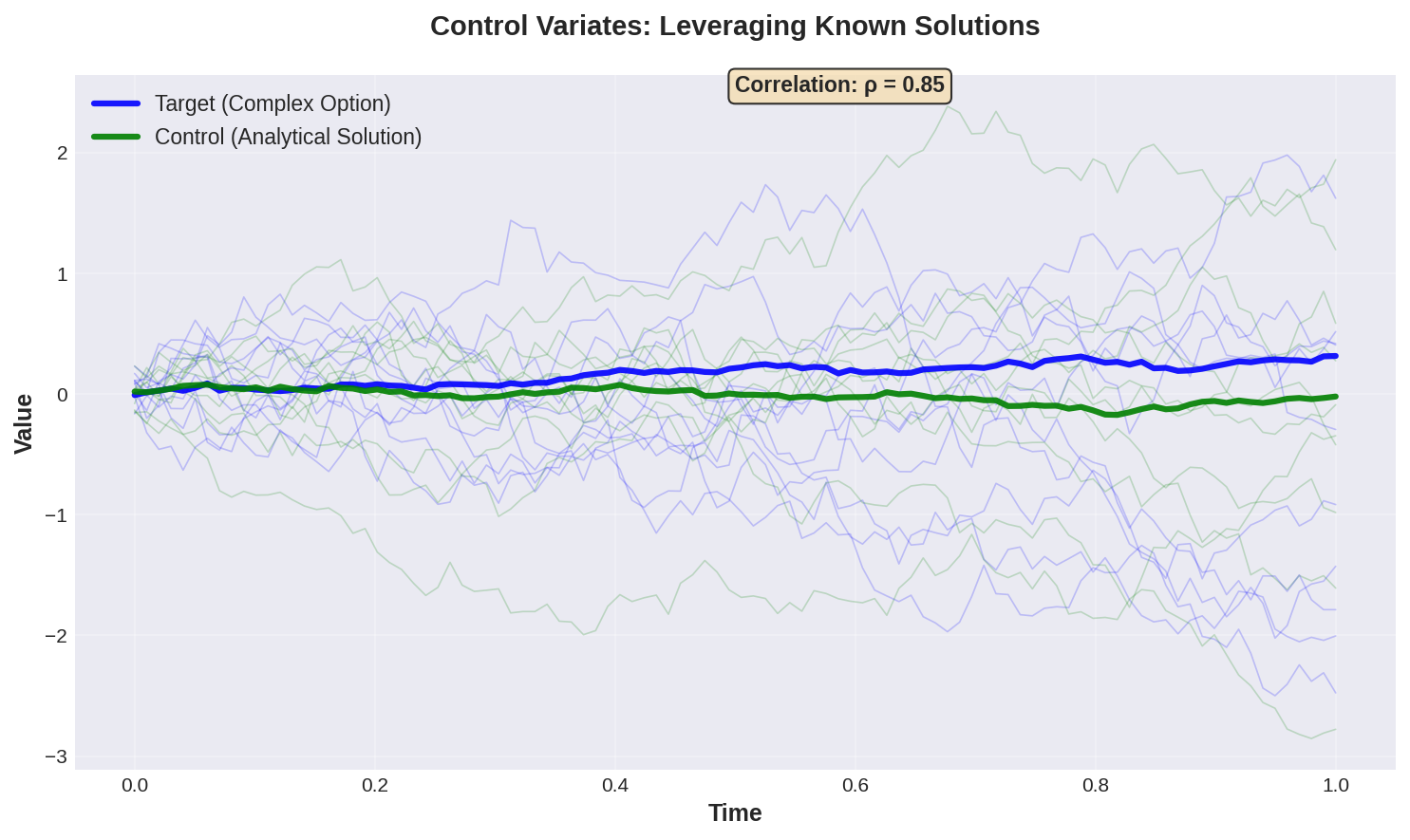

Control variates exploit the availability of analytically tractable approximations. The method involves simulating both the target quantity and a related quantity with a known expected value. The correlation between these quantities allows us to construct a more efficient estimator.

For instance, when pricing Asian options (path-dependent derivatives), we can use geometric Asian options as control variates since they have closed-form solutions. The technique adjusts the Monte Carlo estimate based on the difference between the simulated and analytical values of the control. Properly implemented control variates can achieve variance reductions exceeding 90% in favorable cases.

The effectiveness depends critically on the correlation coefficient between the target and control variables. Financial engineers must carefully select control variates that closely mirror the behavior of the quantity being estimated while remaining analytically tractable.

Importance Sampling: Focusing on Critical Regions

Importance sampling redirects computational effort toward regions of the sample space that contribute most significantly to the final estimate. This proves especially valuable for rare event simulation, such as estimating tail risk or calculating credit value adjustments (CVA) for counterparty risk.

The technique involves sampling from an alternative probability distribution that overweights important regions, then correcting for this bias through likelihood ratios. For example, when estimating the probability of extreme portfolio losses, importance sampling can shift the distribution to make large losses more frequent in the simulation, dramatically reducing the number of samples needed for accurate tail risk estimates.

Selecting an appropriate importance sampling distribution requires domain expertise and often involves iterative refinement. Modern implementations frequently employ adaptive importance sampling, where the sampling distribution evolves based on preliminary simulation results.

Stratified Sampling: Ensuring Representative Coverage

Stratified sampling divides the sample space into non-overlapping strata and samples proportionally from each region. This ensures comprehensive coverage of the entire probability space, preventing the clustering of samples that can occur with pure random sampling.

In financial applications, stratification often occurs along time dimensions or across different market scenarios. For multi-period simulations, stratifying across time steps ensures that each period receives adequate sampling attention. When simulating portfolio returns under various market conditions, stratification across volatility regimes or correlation structures can substantially improve efficiency.

The variance reduction achieved through stratification depends on the homogeneity within strata and heterogeneity between strata. Optimal stratification boundaries can be determined through preliminary analysis or adaptive algorithms.

Quasi-Monte Carlo: Low-Discrepancy Sequences

Quasi-Monte Carlo methods replace pseudo-random numbers with deterministic low-discrepancy sequences, such as Sobol or Halton sequences. These sequences provide more uniform coverage of the sample space than random sampling, leading to faster convergence—often approaching O(1/N) rather than O(1/√N).

For high-dimensional problems common in finance, such as pricing mortgage-backed securities or simulating multi-asset portfolios, quasi-Monte Carlo can deliver order-of-magnitude improvements in efficiency. However, the technique requires careful handling of the effective dimension of the problem. Techniques like principal component analysis or Brownian bridge construction can reduce effective dimensionality and maximize quasi-Monte Carlo benefits.

Implementation Considerations and Best Practices

Successful implementation of variance reduction techniques requires attention to several practical considerations. First, combining multiple techniques often yields compounding benefits, though interactions must be carefully managed. For example, antithetic variates and control variates can be used simultaneously with proper correlation adjustments.

Second, the computational overhead of variance reduction must be weighed against the variance reduction achieved. Some techniques, like importance sampling, require additional calculations per sample. The net efficiency gain depends on whether the variance reduction justifies this overhead.

Third, modern simulation frameworks increasingly incorporate variance reduction automatically. Libraries like QuantLib, Numerix, and proprietary trading systems often provide built-in support for these techniques, though understanding the underlying principles remains essential for optimal configuration and troubleshooting.

Measuring and Validating Efficiency Gains

Quantifying variance reduction effectiveness requires rigorous statistical analysis. The variance reduction factor—the ratio of variances between standard and enhanced methods—provides a direct measure of improvement. However, practitioners should also consider the computational cost per sample and calculate the overall efficiency gain.

Validation should include convergence diagnostics, such as plotting standard errors against sample size on log-log scales to verify improved convergence rates. Cross-validation against analytical solutions or market prices, when available, ensures that variance reduction hasn't introduced bias.

Conclusion

Variance reduction techniques represent essential tools in the quantitative finance toolkit, enabling practical application of Monte Carlo methods to increasingly complex problems. As computational demands grow with model sophistication and regulatory requirements, these techniques become not merely advantageous but necessary. Understanding their theoretical foundations and practical implementation empowers financial engineers to build more efficient, accurate, and scalable simulation systems.

For further exploration, consult the seminal work by Glasserman (2003) on Monte Carlo methods in financial engineering, and explore modern implementations in open-source libraries like QuantLib (https://www.quantlib.org/) and PyQL. The Journal of Computational Finance regularly publishes advances in variance reduction methodology tailored to financial applications.